[ad_1]

Stock market news: The calendar year 2023 has turned out to be a phenomenal year for initial public offerings (IPOs) after a volatile 2022, given improving market conditions. A host of companies from diverse sectors launched their public issues to raise money. Moreover, many others are in the pipeline to go public.

After a bull run in 2021, 2022 brought volatility due to high inflation, rising interest rates, and geopolitical tensions. As a result, many companies scrapped their IPO plans, citing unfavourable market conditions. However, in 2023, the total number of IPO listings has risen sharply and reached the highest level in the past five years, according to Trendlyne.

Source: Trendlyne

Among the slew of issues, Sai Silks (Kalamandir) Ltd (SSKL), a leading apparel retailer in South India, made a quiet debut on the bourses in September. The scrip debuted at a mere 4 per cent premium over the IPO price of Rs 222 on September 27.

Sai Silks’ Rs 1,201 crore IPO was subscribed 4.47 times. The retail portion, however, was subscribed only 0.91 times, whereas the qualified institutional buyer (QIB) portion received a total subscription of 12.17 times.

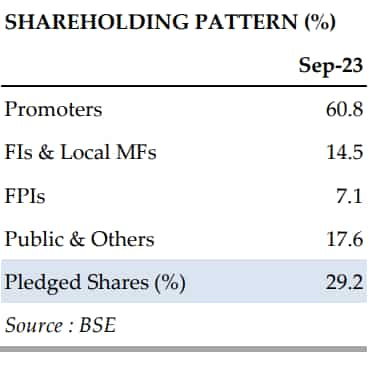

The Hyderabad-based company was founded by Prasad Chalavadi, a techie-turned-entrepreneur, in 2005. It houses four popular brands: Kalamandir (KMR), Kancheepuram, Vara Mahalakshmi Silks (VML), Mandir (MDR), and KLM Fashion Mall (KLM). As of July 31, 2023, the company had a network of 54 stores in four major south Indian states: Andhra Pradesh, Telangana, Karnataka, and Tamil Nadu.

What HDFC Securities says

The migration of retail trade of sarees to organised players from the unorganised sector, the company’s foray into the Tamil Nadu market, improving financials from the COVID-19 blues, and its disciplined expansion approach are some of the key factors that make SSKL’s stock attractive, notes HDFC Securities.

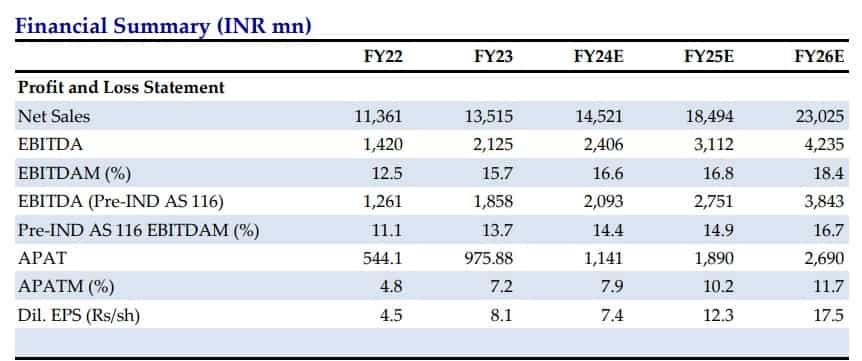

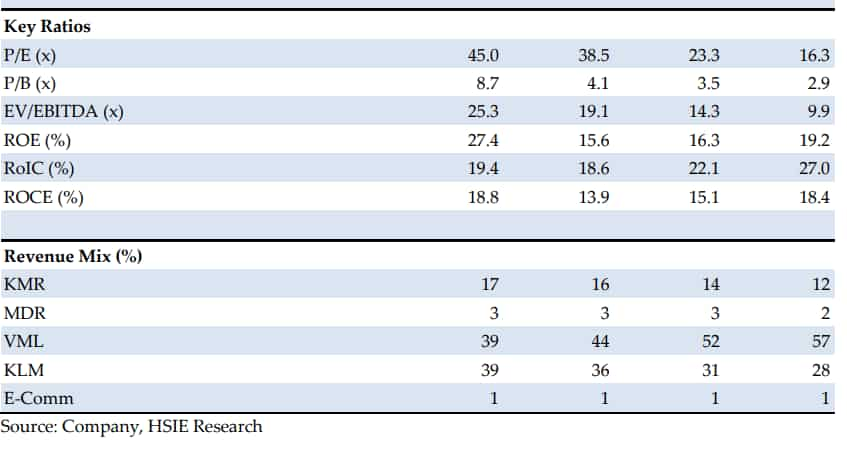

The company’s extremely concentrated expansion approach (FY23 presence: 54 stores; 6,03,414 sq. ft in just 12 southern districts) ensures superior unit economics vis-à-vis most apparel peers (FY20-23 FCF/PAT conversion of 54%; FY20-FY23 average RoCE: 13-14 per cent), highlights Jay Gandhi, a research analyst with HDFC Securities, in a report dated November 23.

The report further highlights that the IPO proceeds will be utilised primarily to expand the more lucrative VML format in Tamil Nadu. The Tamil Nadu market (Rs 74 billion, 32 per cent share in the South) enjoys higher footfall density and consumer affinity for saree purchases. Hence, it is key for all saree brands.

Taking into account these positive triggers, the domestic brokerage has initiated coverage on the stock with a ‘buy’ rating and target price of Rs 385. This translates to a 36 per cent upside from the November 22 closing price.

“We build in sales/EBITDA/PAT CAGRs of 19/27/40% for FY23-26E with average RoCEs of ~16% for FY23-26,” the brokerage said. ROCE stands for return on capital employed.

As regards its financials, HDFC Securities says that SSKL’s growth resilience and product affinity can be seen in its near-complete top-line recovery from the pandemic blues by FY22. In FY23, it continued to improve its performance (up 19 per cent YoY; Rs 13.52 bn; FY16-23 revenue CAGR: 16.7 per cent).

“For FY23–26, we build in a 19 per cent revenue CAGR and an EBITDAM expansion of nearly 300 bps, primarily trickling down from gross margins gains as SSKL earns higher sourcing margins from vendors by offering them better terms of trade and the premiumisation drive continues. 40 per cent profit after tax (PAT) CAGR built with a stable return profile for FY23–26,” it adds.

EBITDAM refers to earnings before interest, income taxes, depreciation, amortisation, and management fees.

Source: HDFC Securities

[ad_2]